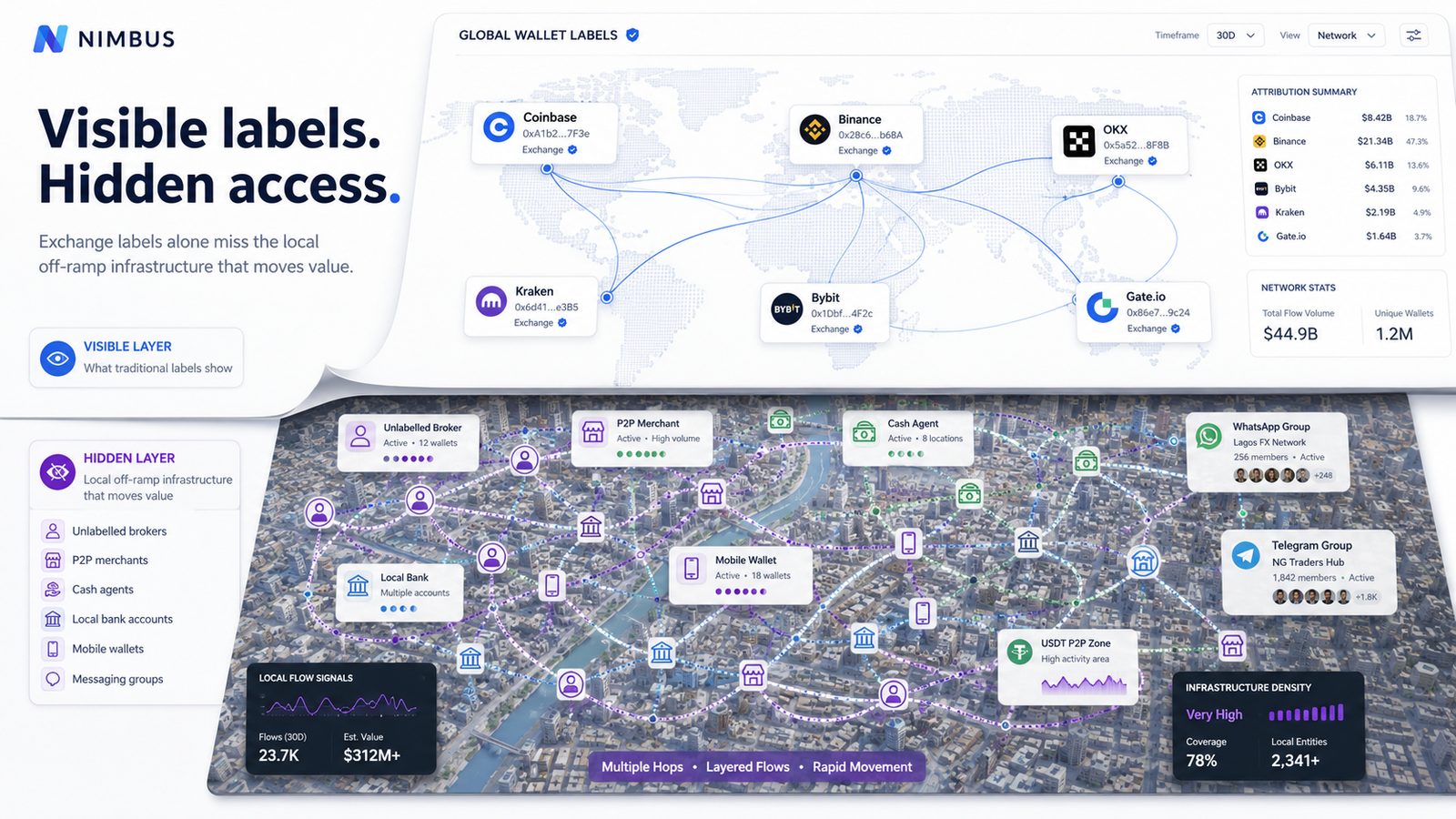

Wallet labels are useful. But in emerging markets, they often fail because the real crypto economy does not fit neatly into global exchange categories.

A wallet label can make blockchain analysis feel more certain than it really is.

An address gets tagged as an exchange.

A cluster gets attached to a known platform.

A service gets grouped under one entity name.

A transaction graph suddenly looks cleaner.

That is the promise of wallet labelling: turning raw blockchain addresses into named infrastructure.

But in emerging markets, the picture is rarely that simple.

Crypto activity often moves through a messy mix of local exchanges, offshore platforms, P2P merchants, Telegram brokers, fintech apps, gambling platforms, OTC desks, remittance agents, payment processors, mule accounts, and deposit-only services.

Some of these actors have formal names and public websites. Many do not. Some use centralised exchanges as backend liquidity. Some rotate wallets constantly. Some operate across multiple countries. Some are only visible through local apps, language-specific groups, or payment instructions inside private chats.

A global wallet label may catch the visible part of the flow.

It often misses the local logic behind it.

That is why wallet labels fail in emerging markets.

Most attribution datasets are strongest where the infrastructure is most visible.

Large global exchanges are easier to identify. They have high-volume wallet clusters, public domains, support pages, compliance teams, and consistent infrastructure patterns. Their wallets appear in many investigations, which gives analysts more chances to confirm and refine labels.

Emerging-market activity is different.

A user in India, Pakistan, Vietnam, Brazil, Nigeria, Turkey, Thailand, Argentina, or South Africa may use a major exchange, but they may also rely on local brokers, P2P merchants, domestic payment apps, remittance shops, offshore exchanges, or informal stablecoin dealers.

Chainalysis’ 2025 Global Crypto Adoption Index ranked India first, followed by the United States, Pakistan, Vietnam, and Brazil, showing that high adoption is not limited to mature Western markets or neatly regulated exchange ecosystems.

That matters for attribution.

A dataset that performs well on Coinbase, Binance, Kraken, OKX, and Bybit may still be weak at identifying a regional broker in Lagos, a Telegram USDT dealer in Istanbul, a small app in São Paulo, or a P2P merchant serving users in Bangkok.

The global exchange label is useful.

It is not the whole map.

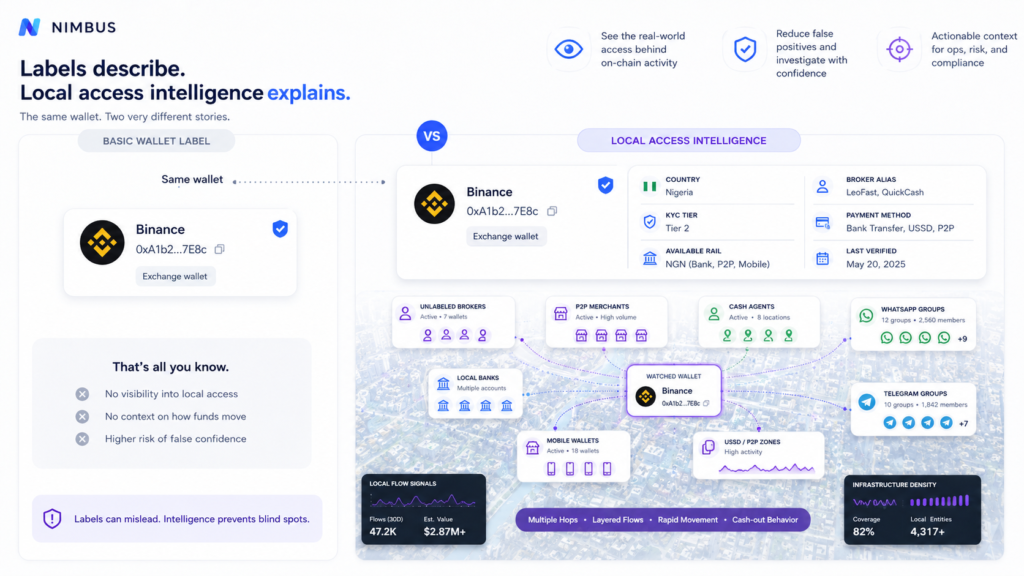

In many markets, the named exchange is not the final intelligence object.

A P2P merchant may use a Binance account. A Telegram broker may source liquidity through OKX. A remittance desk may settle through a local exchange. A small fintech app may use a third-party custodian. A gambling platform may deposit into a larger exchange cluster. A local OTC desk may hold balances across several venues.

On-chain, these flows can collapse into the same familiar labels.

The graph may show funds moving to a major exchange. But the practical actor may be a broker, merchant, mule network, or local cash-out operator using that exchange as infrastructure.

This creates an attribution problem.

The label may be technically correct at one layer, but operationally incomplete.

If the wallet is labelled only as a major exchange, the analyst may miss the local actor who controlled the account, coordinated the deal, received the fiat, or provided the cash-out route.

In emerging markets, the useful question is often not only:

Which platform did the funds touch?

It is:

Who was using that platform as local liquidity infrastructure?

P2P markets create a structural problem for wallet labelling.

In a normal exchange deposit flow, a user sends crypto to a deposit address controlled by the exchange. In a P2P flow, the user may be interacting with another person or merchant, while the platform only provides escrow, reputation, chat, or account infrastructure.

The fiat leg happens outside the blockchain.

A buyer receives USDT. A seller receives local currency through a bank transfer, mobile wallet, cash deposit, or payment app. The blockchain sees the crypto movement, but not the domestic settlement.

This makes labels weaker.

A wallet may belong to a merchant, but the merchant may operate across several platforms. A deposit may be credited inside a centralised exchange, but the economic purpose was a local cash-out. A wallet may look like a personal address, but function as a broker’s working capital wallet.

In markets where P2P is a major liquidity layer, exchange labels alone can hide the real off-ramp.

The address label tells you where the crypto moved.

It does not always tell you how local value changed hands.

Stablecoins made informal exchange activity easier to scale.

A local broker does not need to quote volatile Bitcoin prices all day. They can quote USDT against local currency, take a spread, and settle through domestic payment methods.

This is one reason stablecoin activity has become central to emerging-market crypto use. TRM Labs reported that stablecoins made up 30% of all on-chain crypto transaction volume in 2025, with annual volume reaching more than USD 4 trillion by August 2025. FATF’s 2025 report also noted that fiat-backed stablecoins dominated the stablecoin market, representing 95% of total market capitalisation in October 2025.

For wallet labels, this creates a problem.

High-volume USDT activity may pass through centralised exchanges, self-custody wallets, brokers, P2P merchants, payment intermediaries, and local settlement desks. Some of these are labelled. Many are not.

A stablecoin broker may not have a formal platform name. The “entity” may be a Telegram handle, a WhatsApp number, a repeated bank account, a group admin, or a wallet posted across multiple channels.

Traditional wallet labels are built around identifiable services.

Emerging-market stablecoin liquidity is often built around repeat operators.

That mismatch is where labels fail.

Most global attribution datasets are biased toward what can be repeatedly observed at scale.

That means large exchanges, major bridges, mixers, gambling platforms, and high-profile services get better coverage. Smaller country-specific venues often receive weaker coverage, especially if they operate in local languages, serve only domestic users, require local KYC, or support payment methods that are invisible from outside the market.

This creates predictable blind spots.

A platform may be popular locally but almost invisible globally. A broker may be well known in a Telegram group but absent from a standard VASP list. A fintech app may support crypto deposits indirectly but not present itself as a crypto exchange. A licensed venue may support only a narrow set of rails, while an offshore or informal operator handles far more actual liquidity.

In these cases, the absence of a label does not mean the absence of an entity.

It may only mean the entity sits outside the usual collection path.

Many emerging-market crypto services are difficult to map remotely.

A researcher outside the country may not see the same interface as a local user. Registration may require a domestic phone number. KYC may require national ID. Fiat withdrawals may require a local bank account. P2P markets may display different merchants depending on currency, region, and account status. Some apps may only be available in local app stores.

This affects wallet labels directly.

If an analyst cannot access the local account flow, they may never see the deposit address, payment rail, or withdrawal path that local users actually use.

A support page may claim a rail exists, but only live access proves whether it works. The opposite can also happen: public documentation may be weak, but the rail appears inside the local app after verification.

This is why country-level testing matters.

A wallet label produced from outside the market may be correct in a broad sense, but still miss the account-level infrastructure that local users see.

Even when wallet labels are correct, they are not permanent.

Exchanges rotate deposit addresses. Platforms change custodians. Chains are suspended. Stablecoin rails are added or removed. Withdrawal rules change. KYC requirements tighten. Payment processors are replaced. Apps rebrand. Local operators migrate from one wallet to another.

FATF’s 2025 targeted update on virtual assets and VASPs highlighted continued gaps in global implementation of Recommendation 15, even as jurisdictions with materially important VASP activity made progress in regulation and supervision. That uneven regulatory environment creates constant infrastructure movement. Platforms adapt to local rules, banking relationships, enforcement pressure, and compliance obligations.

In emerging markets, this movement can be faster and less visible.

A label that was accurate six months ago may now be stale. The address may still exist on-chain, but no longer represent active deposit infrastructure. A platform may still operate, but through different rails. A broker may still trade, but from a new wallet. A P2P merchant may still be active, but under a different handle.

A static wallet label cannot capture this unless it includes freshness metadata.

Without a verification date, a label is incomplete.

This is one of the biggest weaknesses.

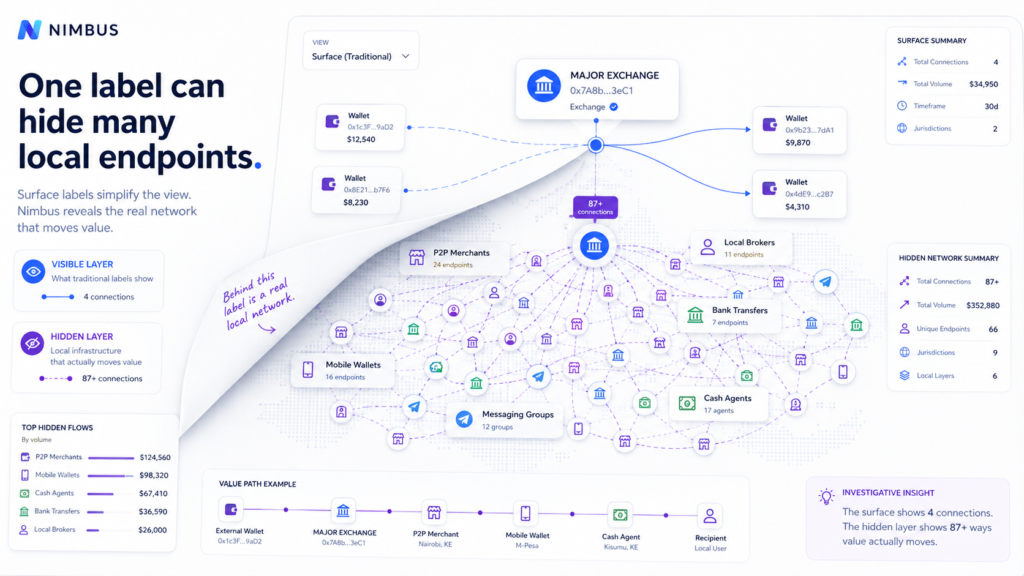

A wallet label usually identifies an entity. But investigations often need to understand a route.

For example, a transaction may involve a local user sending USDT to a broker, the broker consolidating funds into a centralised exchange, and fiat being paid out through a domestic bank transfer. A basic label may only show the centralised exchange.

That is not wrong.

It is just not enough.

The useful route includes the broker, the payment method, the fiat currency, the local country context, the exchange account used for liquidity, and the chain used for settlement.

A venue label answers:

Who controls this wallet or cluster?

A route map answers:

How did value move from crypto into local money?

Emerging-market investigations often need the second answer.

An unknown address forces caution.

A labelled address can create confidence.

That confidence is useful when the label is fresh, precise, and evidence-backed. It is dangerous when the label is stale, broad, or missing local context.

A label like “Exchange” can hide many realities. It may represent a user deposit address, a hot wallet, a third-party custodian, a payment processor, a broker-controlled account, or a regional entity operating under the same brand. It may also represent historical infrastructure that is no longer active.

This can lead to weak conclusions.

An investigator may assume funds reached a compliant exchange when they actually reached an informal broker using that exchange. A compliance system may reduce alert priority because the destination appears familiar. A dataset may undercount exposure to local high-risk services because their flows end inside large exchange clusters.

False confidence creates analytical debt.

It makes bad assumptions look clean.

The fix is not to abandon wallet labels.

The fix is to make them more evidence-backed, local, and time-aware.

A stronger label should include more than an entity name. It should explain how the label was established, when it was last verified, what account conditions applied, which asset and chain were tested, and whether the wallet was linked through direct platform access, transaction evidence, public documentation, OSINT, or behavioural clustering.

For emerging markets, the evidence model should also include local context.

That means capturing whether the address was observed through a local verified account, a P2P merchant flow, a Telegram broker post, a fintech app deposit screen, a gambling platform, an OTC desk, or a remittance route.

A useful record should separate:

This is not just cleaner documentation.

It gives downstream analysts a way to judge how much trust to place in the label.

Wallet labels are only one layer.

The stronger model combines wallet attribution with access intelligence.

That means asking not only which address belongs to which service, but what a user can actually do through that service in a specific market. Can they deposit USDT? Which chain? Can they withdraw crypto? Can they cash out to local bank transfer? Does P2P appear after KYC? Is the rail available to residents only? Is the account deposit-only? Does the platform auto-convert crypto into fiat balance?

This kind of intelligence is harder to collect, but much more useful.

It turns a label from a static tag into a working record of operational access.

For emerging markets, that is the difference between naming infrastructure and understanding it.

Wallet labels fail in emerging markets because emerging-market crypto activity is not only exchange activity.

It is local, fragmented, adaptive, and often mediated through human liquidity networks.

The real ecosystem includes exchanges, P2P merchants, Telegram brokers, OTC desks, fintech apps, payment processors, gambling platforms, remittance agents, domestic banks, mobile wallets, and cash routes. Some are formal. Some are informal. Some are visible globally. Many are not.

A basic wallet label may tell you where funds touched known infrastructure.

It may not tell you who controlled the local route, which payment method was used, whether the rail is still active, whether the platform works in that country, or whether the label is current.

For investigations, that missing context matters.

The question is not only:

What is this wallet labelled as?

It is:

What role does this wallet play in the local movement of value?

That is the question emerging-market attribution has to answer.