Wallet infrastructure rotates, venues change rails, and access rules shift. Static datasets decay.

Blockchain data is permanent. Attribution data is not.

That distinction matters. A transaction hash from three years ago may still point to the same block, same sender, same receiver, and same timestamp. But the meaning attached to that receiver can change. A wallet labelled as an exchange deposit address in 2023 may no longer be active. A venue that once supported TRC20 deposits may have moved users to new addresses. A local broker that once allowed crypto withdrawals may now be deposit-only. A regional exchange may suspend a token, disable a chain, change its KYC rules, or quietly rotate infrastructure without leaving much public signal.

For investigators, compliance teams, Travel Rule providers, and intelligence vendors, this creates a quiet but serious problem: attribution is not a one-time discovery task. It is a freshness problem.

A static dataset may look clean in a spreadsheet. It may include wallet addresses, screenshots, TXIDs, venue names, chains, jurisdictions, and confidence scores. But unless it is periodically re-tested, it starts drifting away from operational reality.

That drift is what makes attribution data go stale.

The base chain records what happened. It does not reliably tell you who controlled the address, whether that address is still active, whether it was assigned to one user or many, whether it belongs to a deposit processor, or whether the venue has since migrated to a new wallet provider.

Attribution sits above the chain. It depends on the moving service layer: exchanges, brokers, payment apps, OTC desks, fintech platforms, gambling venues, P2P rails, custodians, payment processors, and regional liquidity providers.

Those systems are not static. They respond to regulation, liquidity, banking access, wallet vendor changes, chain fees, sanctions exposure, internal risk policy, and user demand.

That is why “this address belonged to this venue” is not the same as “this address still represents this venue today”.

Many services rotate deposit addresses for operational, security, or infrastructure reasons. Sometimes this happens at the user level. Sometimes it happens at the chain level. Sometimes it happens because a venue changes custody providers, updates wallet architecture, or retires older deposit addresses.

This is not theoretical. Exchanges and regional platforms regularly publish notices about deposit address changes, token migrations, suspended deposits, withdrawals, or delistings. For example, MaiCoin announced that old TRC20-USDT deposit addresses generated before a certain date would only be supported until a stated deadline, while Binance TH announced deposit and withdrawal suspension around a token swap and rebrand process.

For attribution teams, this creates three failure modes.

First, an old address may still be historically correct but operationally dead. It is valid for past investigations, but useless for current access mapping.

Second, a new address may exist that is not yet in the dataset. This creates blind spots in transaction monitoring and entity graph enrichment.

Third, the dataset may contain both old and new infrastructure without clearly separating historical attribution from currently verified attribution.

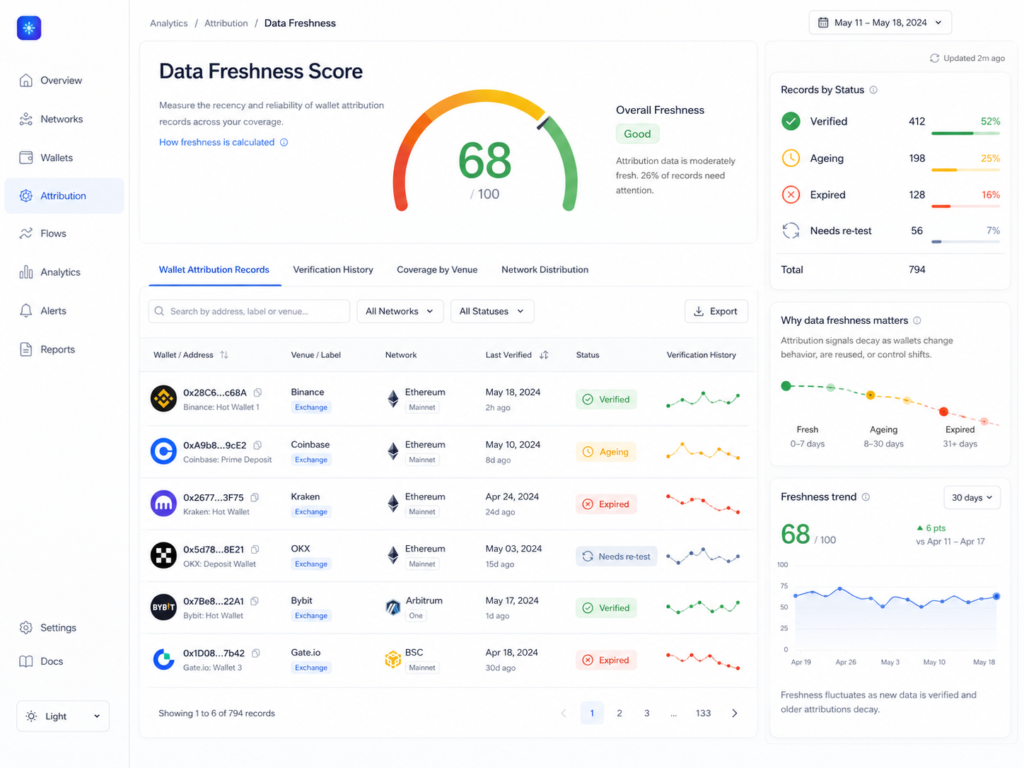

That last point is important. A serious attribution system should not only answer “who was this?” It should answer “when was this verified?”, “through what method?”, and “is this still active?”

Without freshness metadata, attribution becomes archaeology.

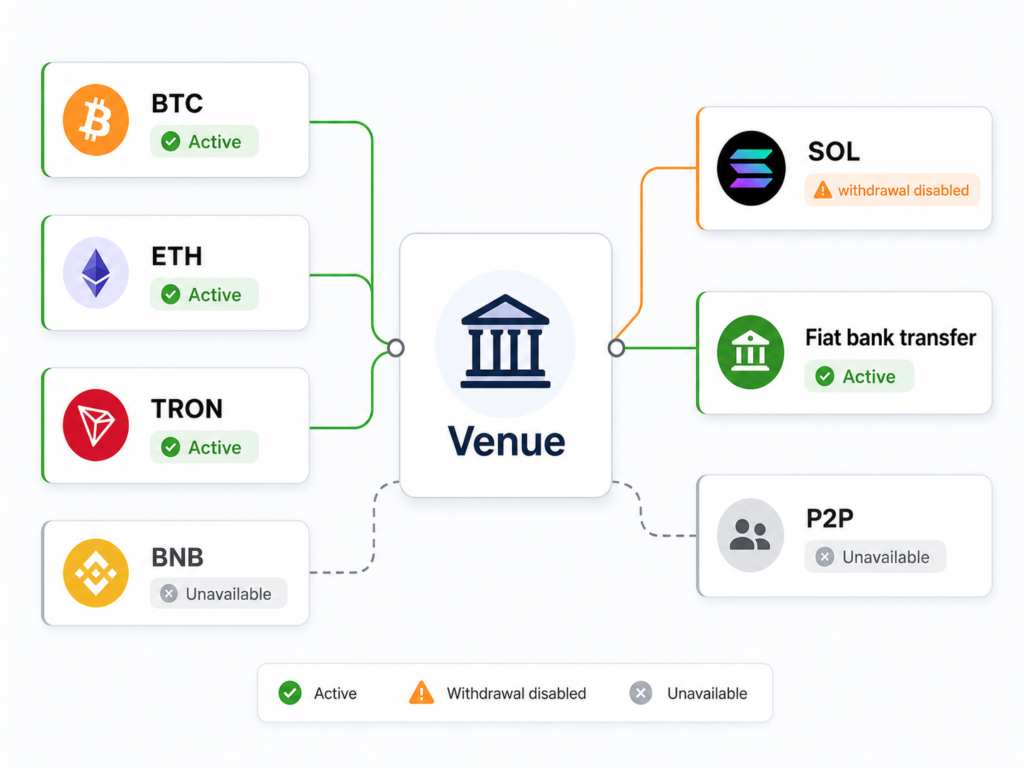

Crypto venues do not support all chains equally forever. They add networks. They remove networks. They suspend deposits. They disable withdrawals. They switch from one stablecoin rail to another. They may support a token on one network for deposits, but not for withdrawals. They may support crypto deposits, but auto-convert into fiat balance. They may allow domestic users to access more rails than foreign users. They may expose different rails depending on jurisdiction, KYC tier, asset, or app version.

This matters because attribution is not just about names and addresses. It is about functional access.

A venue that supports USDT-TRC20, ETH, BNB, SOL, and BTC is not operationally equivalent to a venue that only supports USDT deposits with no crypto withdrawal. Both may appear as “crypto platforms” in a country inventory, but their intelligence value is different.

Deposit and withdrawal policies are dynamic. Crypto.com’s exchange support pages, for example, treat deposits and withdrawals as operational settings involving fees, limits, and processing times, which can vary by asset and transfer type.

For investigators, this affects the quality of conclusions.

If a dataset says “Venue X supports USDT”, that is incomplete. The useful questions are:

Does it support USDT deposits?

Which networks?

Does it support withdrawals?

Are withdrawals crypto-native or fiat-only?

Are rails available after KYC?

Are they available in the target country?

Are they active today?

Static labels flatten these distinctions. Fresh attribution preserves them.

A venue may be accessible from one country but not another. It may allow account creation but block deposits. It may allow deposits but require enhanced KYC for withdrawals. It may offer different payment methods to residents, foreigners, companies, and high-volume users.

This is especially relevant in emerging markets, where the practical crypto landscape often differs from the formal regulatory landscape.

A country may have licensed exchanges, globally accessible offshore exchanges, fintech apps with crypto exposure, informal OTC brokers, P2P marketplaces, casino rails, and tokenised investment platforms operating in parallel. Some are regulated. Some are tolerated. Some are blocked intermittently. Some are usable only through local identity, domestic bank accounts, local phone numbers, or region-specific app stores.

Public data rarely captures this properly.

A platform’s website may say it supports a country. But live access may reveal something else. Registration may work, but KYC may fail. KYC may pass, but deposits may not show. Deposits may work, but withdrawals may require local banking rails. Withdrawal options may appear only after a successful micro-deposit. Some rails may exist in the interface but fail during execution.

This is where live account-based verification becomes materially different from desk research.

A stale dataset might preserve the public claim. A fresh dataset captures the operational truth.

Crypto attribution sits inside a regulatory environment that keeps changing.

FATF continues to pressure jurisdictions on virtual asset supervision, Travel Rule implementation, offshore VASP risks, and stablecoin-related illicit finance exposure. Its 2025 targeted update highlights the importance of licensing, registration, and risk-based supervision of virtual asset service providers.

Regulatory pressure changes venue behaviour.

Some platforms tighten onboarding. Some exit markets. Some remove privacy-sensitive assets. Some disable high-risk jurisdictions. Some restrict stablecoin rails. Some move from open global access to region-specific entities. Some introduce stricter withdrawal checks. Some rely more heavily on third-party custody, compliance vendors, or Travel Rule integrations.

For attribution datasets, this means jurisdictional assumptions decay quickly.

A platform that was accessible in Thailand, Nigeria, Brazil, India, or Vietnam six months ago may not behave the same way today. Even if the domain still loads, the underlying access path may have changed.

This is why jurisdictional freshness matters. A wallet attribution record without country-level access context is often too shallow for real investigative use.

Illicit actors adapt to enforcement pressure. They move across chains, assets, exchanges, payment apps, bridges, mixers, nested services, OTC brokers, gambling venues, and informal cash-out points.

Chainalysis has repeatedly reported that crypto crime is not limited to one asset or one type of service, and that different categories of illicit activity use different cash-out behaviours. Its 2025 reporting notes that scams and laundering activity often spread across a mix of asset types, while some other categories remain more Bitcoin-heavy.

That matters for attribution freshness because today’s relevant off-ramp may not be yesterday’s relevant off-ramp.

A country’s active crypto cash-out ecosystem can shift because of enforcement, banking access, local liquidity, app popularity, sanctions pressure, or simple user migration. A small broker or regional exchange can become important before it appears in mainstream datasets. A large global exchange can become less useful in a specific country if local rails weaken. A payment app can become a practical bridge even if it is not formally labelled as a crypto exchange.

If attribution only tracks known major venues, it misses where activity actually moves.

Bad attribution does not only create blind spots. It also creates false positives.

A stale label can make a legitimate transaction look suspicious. It can also make a risky transaction look cleaner than it is. Both outcomes waste analyst time and weaken confidence in the dataset.

Elliptic describes accurate attribution as a way to reduce false positives by distinguishing legitimate activity from genuinely high-risk behaviour.

The inverse is also true: stale attribution increases noise.

If an old wallet cluster remains labelled as an active exchange hot wallet, screening systems may over-alert. If a service has changed infrastructure and the new addresses are missing, monitoring systems may under-alert. If a deposit-only fintech app is labelled the same way as a full withdrawal-enabled exchange, risk teams may misunderstand the actual flow of funds.

Fresh attribution is not just about coverage. It is about precision.

A screenshot proves what was visible at one point in time. A spreadsheet records what someone knew when the sheet was created. Both are useful, but neither is enough on its own.

Attribution needs evidence. But evidence also needs lifecycle management.

A strong attribution bundle should include:

The expiry window is the part many datasets miss.

Not all attribution records age at the same speed. A major exchange hot wallet may remain useful for longer. A regional platform’s TRC20 deposit infrastructure may change faster. A P2P broker’s payment flow may decay even faster. A fintech app’s access model may change after one compliance update.

The dataset should reflect this.

The better model is not a static country file. It is a living attribution layer.

That means three things.

First, attribution records need timestamps and evidence trails. A label without verification history is just a claim.

Second, datasets need re-verification cycles. Monthly, quarterly, or event-triggered checks can identify when venues rotate wallets, suspend chains, change access, or introduce new rails.

Third, coverage should prioritise practical importance, not just public visibility. The most useful venues are often the ones that matter locally: the exchange people actually use, the broker that supports local banks, the offshore app that still works, the fintech platform that quietly routes deposits, or the regional venue missing from global datasets.

This is especially true in emerging markets, where crypto usage often sits between formal exchanges, informal brokers, payment apps, P2P liquidity, and offshore services.

A static list cannot capture that. A live verification network can.

Attribution data decays because the crypto service layer is alive.

Wallets rotate. Rails change. Venues rebrand. Chains get added or removed. KYC rules tighten. Local access shifts. Regulations change. Criminal flows adapt. Apps update. Deposit addresses expire. Withdrawal paths disappear.

The blockchain keeps the old facts intact. But intelligence work depends on current meaning.

For compliance teams, stale attribution creates false positives and missed risk. For investigators, it creates broken assumptions. For Travel Rule and VASP discovery teams, it weakens entity resolution. For analytics vendors, it turns coverage into a liability if the freshness layer is not visible.

The answer is not bigger spreadsheets. It is evidence-backed, timestamped, country-level, re-verifiable attribution.

In crypto investigations, the question is rarely just “who owned this wallet?”

The better question is:

When did we last prove it?