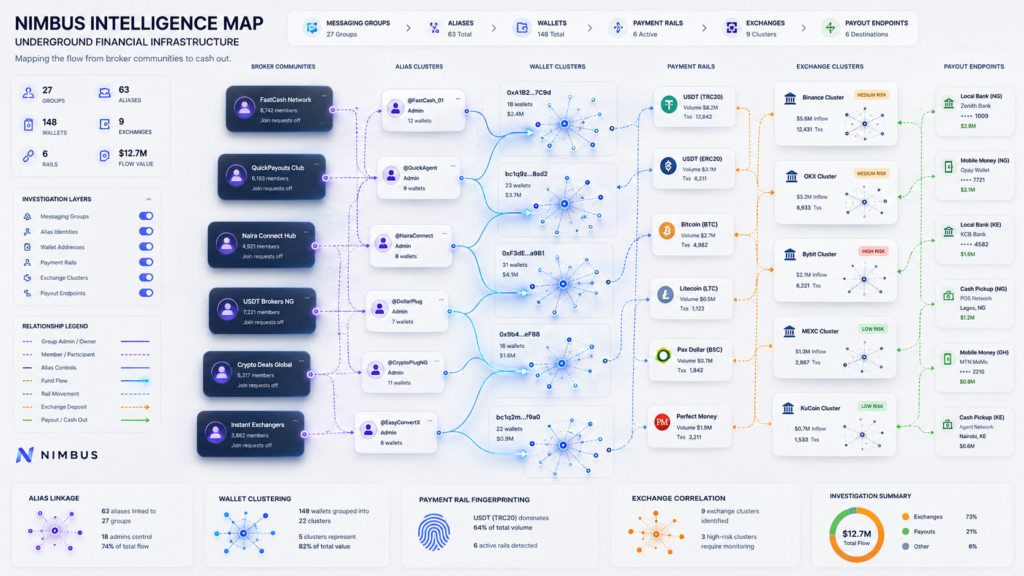

Not every crypto off-ramp has a website, order book, or compliance contact. Some of the most important liquidity routes operate through people, chat groups, aliases, and local payment rails.

Crypto investigations usually start with visible infrastructure.

Centralised exchanges.

Known deposit wallets.

Custodial clusters.

Licensed VASPs.

Exchange hot wallets.

Publicly documented payment rails.

That is the clean layer.

But in many markets, especially where banking access is fragmented, capital controls exist, or stablecoin liquidity is high, the real off-ramp layer is messier. Users do not always cash out through formal exchanges. They use P2P merchants, OTC brokers, Telegram dealers, WhatsApp groups, local payment agents, mule networks, informal remittance routes, and semi-public chat-based exchanges.

This layer is harder to map because it does not behave like a normal platform.

It is human, local, adaptive, and often semi-invisible.

For investigators, this creates a major blind spot.

The blockchain may show funds moving into a wallet. But the cash-out logic may be happening in Telegram.

Most people think of P2P as an exchange feature.

That is partly true. Many exchanges offer P2P marketplaces where users buy and sell crypto directly with each other, while fiat settlement happens through local bank transfer, mobile wallet, cash deposit, or another domestic payment method.

But in practice, P2P is bigger than the exchange interface.

It behaves like distributed local liquidity infrastructure.

A P2P merchant can:

The exchange may only be the matching layer. The real liquidity relationship often continues elsewhere.

This matters because P2P merchants can become repeat off-ramp points. A user sends crypto. The merchant pays fiat. The blockchain sees only the crypto leg. The domestic payment leg disappears into bank transfers, mobile wallets, or cash.

That is why P2P mapping is not optional.

It is one of the missing layers between on-chain tracing and real-world money movement.

Telegram-based crypto exchange groups are not all the same.

Some are informal local broker groups. Some are OTC desks. Some are P2P liquidity channels. Some are scam groups. Some are laundering networks. Some are marketplaces where users buy and sell access, accounts, payment services, stolen data, mule accounts, SIM cards, or crypto liquidity.

The form can vary, but the operating pattern is similar:

This layer is useful precisely because it is flexible.

A Telegram exchange can change wallets quickly. It can migrate channels. It can rename admins. It can move from one stablecoin chain to another. It can use new mule accounts. It can split larger flows across several counterparties. It can serve users who cannot or do not want to use regulated platforms.

For investigators, this makes Telegram exchanges difficult but valuable.

They often expose the operational layer behind the address.

Stablecoins turned informal crypto exchange into a cleaner business.

Bitcoin is volatile. Stablecoins are easier to quote.

A local dealer can quote:

No one has to price a volatile asset every few minutes. The dealer only needs a spread, a payment method, and available liquidity.

That is why stablecoin-heavy P2P and Telegram exchange activity matters for country-level attribution.

USDT, especially on low-cost networks like TRON, is widely used for fast settlement in informal liquidity routes. Elliptic has reported that large Telegram-based illicit marketplaces serving fraud networks in Southeast Asia used USDT as the primary payment method, with Huione Guarantee linked to at least $24 billion in transactions and Xinbi Guarantee linked to $8.4 billion.

Those examples are extreme. Most P2P and Telegram brokers are not operating at that scale.

But they show the broader point: chat-based crypto liquidity can become major financial infrastructure without looking like a normal exchange.

On-chain data shows addresses and flows.

Telegram groups can reveal:

This does not replace blockchain analysis. It enriches it.

A wallet that looks like an unknown address on-chain may become meaningful when it appears in a Telegram group offering USDT cash-out in a specific country.

A cluster that looks like generic high-volume stablecoin activity may become a local broker network once its handles, payment methods, and counterparties are mapped.

A P2P merchant may appear as one account inside a formal exchange, but operate across several chat groups outside it.

This is where OSINT and blockchain attribution need to meet.

The address is only one part of the evidence. The surrounding human infrastructure gives it context.

The formal crypto industry likes clean categories:

The local off-ramp world is less tidy.

A Telegram broker may act like an OTC desk for large trades, a P2P merchant for small trades, a remittance agent for cross-border settlement, and a liquidity source for local cash-out.

A P2P merchant on an exchange may also operate private Telegram deals.

An informal exchange group may use wallets at several centralised exchanges to manage liquidity.

A “broker” may simply be someone with verified accounts, local bank access, and enough stablecoin inventory.

For investigations, the question is not “which formal category does this entity belong to?”

The better question is:

What function does this actor perform in the flow of funds?

They may perform one or more functions:

This functional view is more useful than formal taxonomy.

Telegram-based crypto markets are adaptive.

When one group is removed, users can migrate. When one marketplace is disrupted, another can absorb activity. When admins are banned, replacement channels can appear. When a wallet is exposed, new wallets can be posted.

Reuters reported in May 2025 that Telegram shut down two major Chinese-language digital black markets, Xinbi Guarantee and Huione Guarantee, after they had reportedly facilitated more than $35 billion in transactions since 2021.

Elliptic later reported that after Huione Guarantee was shut down, merchants were encouraged to switch to another Telegram-based market called Tudou Guarantee, showing how quickly activity can attempt to relocate.

This is the core problem with static mapping.

A formal exchange usually has a domain, brand, legal entity, and infrastructure footprint. A Telegram market has looser boundaries. It may exist as channels, admins, merchant handles, wallet addresses, invite links, language communities, escrow relationships, and payment instructions.

To map it properly, investigators need to track both on-chain and off-chain signals.

P2P transactions are difficult because the fiat leg is not on-chain.

A simplified flow may look like this:

On-chain, investigators may only see:

They may not see:

That gap is where attribution weakens.

P2P and Telegram mapping help close it by tying wallets to actors, aliases, regions, payment rails, and repeated behavioural patterns.

P2P and Telegram exchanges are especially relevant where formal rails are weak or inconvenient.

This includes markets with:

In these markets, users may not ask, “Which regulated exchange is best?”

They ask:

Those questions shape the real off-ramp map.

The most important actor may not be the most visible platform. It may be the broker everyone uses.

You cannot map Telegram-based exchange activity the same way you map a centralised exchange.

A centralised exchange record may focus on:

A Telegram exchange record needs additional fields:

This record should clearly separate observation from verification.

For example:

That level of precision prevents overclaiming.

This distinction matters.

P2P and Telegram exchanges can be used for lawful purposes, especially in countries where formal banking and exchange infrastructure is weak.

People may use informal crypto brokers for:

But the same rails can also be exploited for:

The role of intelligence is not to label every informal broker as criminal.

The role is to map function, risk, evidence, and context.

A Telegram broker with transparent reputation, stable local payment methods, and normal retail flow is different from a broker advertising laundering services, mule accounts, scam cash-out, or anonymity guarantees.

The map should preserve that distinction.

P2P and Telegram exchange mapping should focus on recurring signals.

Important indicators include:

These signals do not automatically prove illicit activity. They guide prioritisation.

For a country-level attribution dataset, P2P and Telegram exchange coverage adds a layer that formal exchange mapping cannot provide.

It helps answer:

This is especially useful for:

Formal exchange attribution tells you where funds may have entered a known service.

P2P and Telegram mapping tells you how funds may have moved into local liquidity.

Crypto investigations are cleanest on-chain.

They become harder at the edge.

That edge is where a wallet becomes a person, broker, merchant, mule account, bank transfer, mobile wallet, cash pickup, or Telegram handle.

P2P and Telegram exchanges live at that edge.

They are not always visible in formal registries. They may not have websites. They may not have compliance departments. They may not expose stable infrastructure. But they can still move large volumes, connect users to local fiat, and act as the practical off-ramp in markets where formal exchange coverage is incomplete.

The investigation does not end when funds leave the blockchain graph.

Often, that is where the most important map begins.

The real question is not only:

Which exchange did the funds reach?

It is:

Who turned the crypto into local money?

That is the hidden role of P2P and Telegram exchanges.