Wallet infrastructure rotates, venues change rails, and access rules shift. Static datasets decay.

Blockchain data is permanent. Attribution data is not.

That distinction matters. A transaction hash from three years ago may still point to the same block, same sender, same receiver, and same timestamp. But the meaning attached to that receiver can change. A wallet labelled as an exchange deposit address in 2023 may no longer be active. A venue that once supported TRC20 deposits may have moved users to new addresses. A local broker that once allowed crypto withdrawals may now be deposit-only. A regional exchange may suspend a token, disable a chain, change its KYC rules, or quietly rotate infrastructure without leaving much public signal.

For investigators, compliance teams, Travel Rule providers, and intelligence vendors, this creates a quiet but serious problem: attribution is not a one-time discovery task. It is a freshness problem.

A static dataset may look clean in a spreadsheet. It may include wallet addresses, screenshots, TXIDs, venue names, chains, jurisdictions, and confidence scores. But unless it is periodically re-tested, it starts drifting away from operational reality.

That drift is what makes attribution data go stale.

The base chain records what happened. It does not reliably tell you who controlled the address, whether that address is still active, whether it was assigned to one user or many, whether it belongs to a deposit processor, or whether the venue has since migrated to a new wallet provider.

Attribution sits above the chain. It depends on the moving service layer: exchanges, brokers, payment apps, OTC desks, fintech platforms, gambling venues, P2P rails, custodians, payment processors, and regional liquidity providers.

Those systems are not static. They respond to regulation, liquidity, banking access, wallet vendor changes, chain fees, sanctions exposure, internal risk policy, and user demand.

That is why “this address belonged to this venue” is not the same as “this address still represents this venue today”.

Many services rotate deposit addresses for operational, security, or infrastructure reasons. Sometimes this happens at the user level. Sometimes it happens at the chain level. Sometimes it happens because a venue changes custody providers, updates wallet architecture, or retires older deposit addresses.

This is not theoretical. Exchanges and regional platforms regularly publish notices about deposit address changes, token migrations, suspended deposits, withdrawals, or delistings. For example, MaiCoin announced that old TRC20-USDT deposit addresses generated before a certain date would only be supported until a stated deadline, while Binance TH announced deposit and withdrawal suspension around a token swap and rebrand process.

For attribution teams, this creates three failure modes.

First, an old address may still be historically correct but operationally dead. It is valid for past investigations, but useless for current access mapping.

Second, a new address may exist that is not yet in the dataset. This creates blind spots in transaction monitoring and entity graph enrichment.

Third, the dataset may contain both old and new infrastructure without clearly separating historical attribution from currently verified attribution.

That last point is important. A serious attribution system should not only answer “who was this?” It should answer “when was this verified?”, “through what method?”, and “is this still active?”

Without freshness metadata, attribution becomes archaeology.

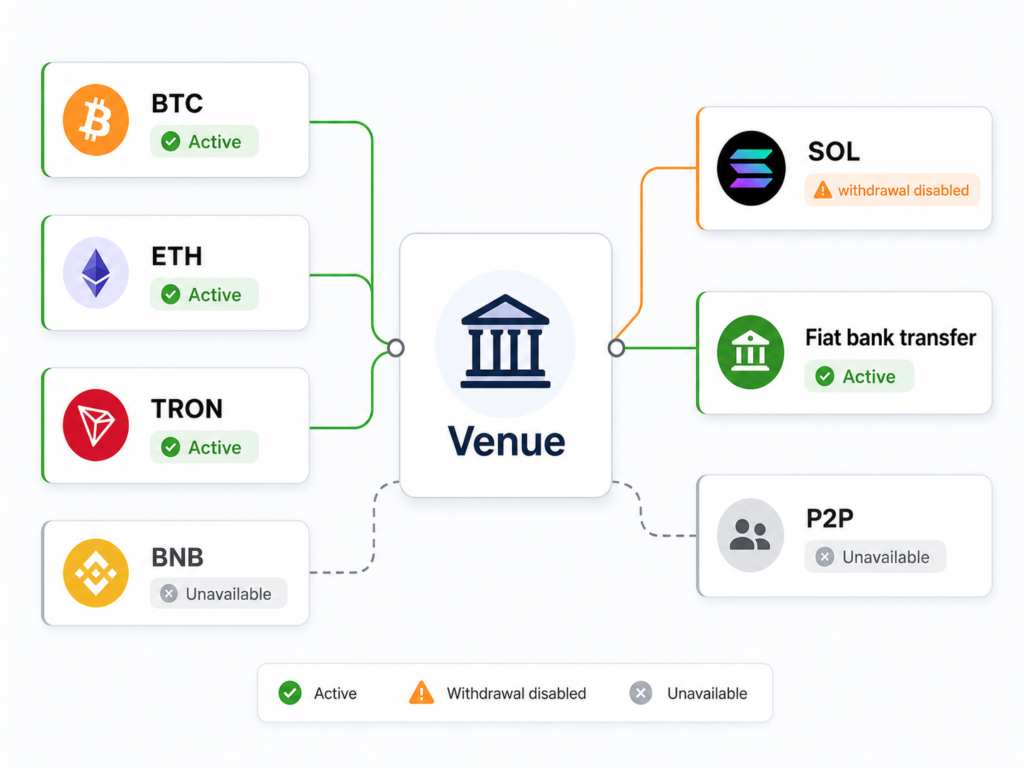

Crypto venues do not support all chains equally forever. They add networks. They remove networks. They suspend deposits. They disable withdrawals. They switch from one stablecoin rail to another. They may support a token on one network for deposits, but not for withdrawals. They may support crypto deposits, but auto-convert into fiat balance. They may allow domestic users to access more rails than foreign users. They may expose different rails depending on jurisdiction, KYC tier, asset, or app version.

This matters because attribution is not just about names and addresses. It is about functional access.

A venue that supports USDT-TRC20, ETH, BNB, SOL, and BTC is not operationally equivalent to a venue that only supports USDT deposits with no crypto withdrawal. Both may appear as “crypto platforms” in a country inventory, but their intelligence value is different.

Deposit and withdrawal policies are dynamic. Crypto.com’s exchange support pages, for example, treat deposits and withdrawals as operational settings involving fees, limits, and processing times, which can vary by asset and transfer type.

For investigators, this affects the quality of conclusions.

If a dataset says “Venue X supports USDT”, that is incomplete. The useful questions are:

Does it support USDT deposits?

Which networks?

Does it support withdrawals?

Are withdrawals crypto-native or fiat-only?

Are rails available after KYC?

Are they available in the target country?

Are they active today?

Static labels flatten these distinctions. Fresh attribution preserves them.

A venue may be accessible from one country but not another. It may allow account creation but block deposits. It may allow deposits but require enhanced KYC for withdrawals. It may offer different payment methods to residents, foreigners, companies, and high-volume users.

This is especially relevant in emerging markets, where the practical crypto landscape often differs from the formal regulatory landscape.

A country may have licensed exchanges, globally accessible offshore exchanges, fintech apps with crypto exposure, informal OTC brokers, P2P marketplaces, casino rails, and tokenised investment platforms operating in parallel. Some are regulated. Some are tolerated. Some are blocked intermittently. Some are usable only through local identity, domestic bank accounts, local phone numbers, or region-specific app stores.

Public data rarely captures this properly.

A platform’s website may say it supports a country. But live access may reveal something else. Registration may work, but KYC may fail. KYC may pass, but deposits may not show. Deposits may work, but withdrawals may require local banking rails. Withdrawal options may appear only after a successful micro-deposit. Some rails may exist in the interface but fail during execution.

This is where live account-based verification becomes materially different from desk research.

A stale dataset might preserve the public claim. A fresh dataset captures the operational truth.

Crypto attribution sits inside a regulatory environment that keeps changing.

FATF continues to pressure jurisdictions on virtual asset supervision, Travel Rule implementation, offshore VASP risks, and stablecoin-related illicit finance exposure. Its 2025 targeted update highlights the importance of licensing, registration, and risk-based supervision of virtual asset service providers.

Regulatory pressure changes venue behaviour.

Some platforms tighten onboarding. Some exit markets. Some remove privacy-sensitive assets. Some disable high-risk jurisdictions. Some restrict stablecoin rails. Some move from open global access to region-specific entities. Some introduce stricter withdrawal checks. Some rely more heavily on third-party custody, compliance vendors, or Travel Rule integrations.

For attribution datasets, this means jurisdictional assumptions decay quickly.

A platform that was accessible in Thailand, Nigeria, Brazil, India, or Vietnam six months ago may not behave the same way today. Even if the domain still loads, the underlying access path may have changed.

This is why jurisdictional freshness matters. A wallet attribution record without country-level access context is often too shallow for real investigative use.

Illicit actors adapt to enforcement pressure. They move across chains, assets, exchanges, payment apps, bridges, mixers, nested services, OTC brokers, gambling venues, and informal cash-out points.

Chainalysis has repeatedly reported that crypto crime is not limited to one asset or one type of service, and that different categories of illicit activity use different cash-out behaviours. Its 2025 reporting notes that scams and laundering activity often spread across a mix of asset types, while some other categories remain more Bitcoin-heavy.

That matters for attribution freshness because today’s relevant off-ramp may not be yesterday’s relevant off-ramp.

A country’s active crypto cash-out ecosystem can shift because of enforcement, banking access, local liquidity, app popularity, sanctions pressure, or simple user migration. A small broker or regional exchange can become important before it appears in mainstream datasets. A large global exchange can become less useful in a specific country if local rails weaken. A payment app can become a practical bridge even if it is not formally labelled as a crypto exchange.

If attribution only tracks known major venues, it misses where activity actually moves.

Bad attribution does not only create blind spots. It also creates false positives.

A stale label can make a legitimate transaction look suspicious. It can also make a risky transaction look cleaner than it is. Both outcomes waste analyst time and weaken confidence in the dataset.

Elliptic describes accurate attribution as a way to reduce false positives by distinguishing legitimate activity from genuinely high-risk behaviour.

The inverse is also true: stale attribution increases noise.

If an old wallet cluster remains labelled as an active exchange hot wallet, screening systems may over-alert. If a service has changed infrastructure and the new addresses are missing, monitoring systems may under-alert. If a deposit-only fintech app is labelled the same way as a full withdrawal-enabled exchange, risk teams may misunderstand the actual flow of funds.

Fresh attribution is not just about coverage. It is about precision.

A screenshot proves what was visible at one point in time. A spreadsheet records what someone knew when the sheet was created. Both are useful, but neither is enough on its own.

Attribution needs evidence. But evidence also needs lifecycle management.

A strong attribution bundle should include:

The expiry window is the part many datasets miss.

Not all attribution records age at the same speed. A major exchange hot wallet may remain useful for longer. A regional platform’s TRC20 deposit infrastructure may change faster. A P2P broker’s payment flow may decay even faster. A fintech app’s access model may change after one compliance update.

The dataset should reflect this.

The better model is not a static country file. It is a living attribution layer.

That means three things.

First, attribution records need timestamps and evidence trails. A label without verification history is just a claim.

Second, datasets need re-verification cycles. Monthly, quarterly, or event-triggered checks can identify when venues rotate wallets, suspend chains, change access, or introduce new rails.

Third, coverage should prioritise practical importance, not just public visibility. The most useful venues are often the ones that matter locally: the exchange people actually use, the broker that supports local banks, the offshore app that still works, the fintech platform that quietly routes deposits, or the regional venue missing from global datasets.

This is especially true in emerging markets, where crypto usage often sits between formal exchanges, informal brokers, payment apps, P2P liquidity, and offshore services.

A static list cannot capture that. A live verification network can.

Attribution data decays because the crypto service layer is alive.

Wallets rotate. Rails change. Venues rebrand. Chains get added or removed. KYC rules tighten. Local access shifts. Regulations change. Criminal flows adapt. Apps update. Deposit addresses expire. Withdrawal paths disappear.

The blockchain keeps the old facts intact. But intelligence work depends on current meaning.

For compliance teams, stale attribution creates false positives and missed risk. For investigators, it creates broken assumptions. For Travel Rule and VASP discovery teams, it weakens entity resolution. For analytics vendors, it turns coverage into a liability if the freshness layer is not visible.

The answer is not bigger spreadsheets. It is evidence-backed, timestamped, country-level, re-verifiable attribution.

In crypto investigations, the question is rarely just “who owned this wallet?”

The better question is:

When did we last prove it?

Not every crypto off-ramp has a website, order book, or compliance contact. Some of the most important liquidity routes operate through people, chat groups, aliases, and local payment rails.

Crypto investigations usually start with visible infrastructure.

Centralised exchanges.

Known deposit wallets.

Custodial clusters.

Licensed VASPs.

Exchange hot wallets.

Publicly documented payment rails.

That is the clean layer.

But in many markets, especially where banking access is fragmented, capital controls exist, or stablecoin liquidity is high, the real off-ramp layer is messier. Users do not always cash out through formal exchanges. They use P2P merchants, OTC brokers, Telegram dealers, WhatsApp groups, local payment agents, mule networks, informal remittance routes, and semi-public chat-based exchanges.

This layer is harder to map because it does not behave like a normal platform.

It is human, local, adaptive, and often semi-invisible.

For investigators, this creates a major blind spot.

The blockchain may show funds moving into a wallet. But the cash-out logic may be happening in Telegram.

Most people think of P2P as an exchange feature.

That is partly true. Many exchanges offer P2P marketplaces where users buy and sell crypto directly with each other, while fiat settlement happens through local bank transfer, mobile wallet, cash deposit, or another domestic payment method.

But in practice, P2P is bigger than the exchange interface.

It behaves like distributed local liquidity infrastructure.

A P2P merchant can:

The exchange may only be the matching layer. The real liquidity relationship often continues elsewhere.

This matters because P2P merchants can become repeat off-ramp points. A user sends crypto. The merchant pays fiat. The blockchain sees only the crypto leg. The domestic payment leg disappears into bank transfers, mobile wallets, or cash.

That is why P2P mapping is not optional.

It is one of the missing layers between on-chain tracing and real-world money movement.

Telegram-based crypto exchange groups are not all the same.

Some are informal local broker groups. Some are OTC desks. Some are P2P liquidity channels. Some are scam groups. Some are laundering networks. Some are marketplaces where users buy and sell access, accounts, payment services, stolen data, mule accounts, SIM cards, or crypto liquidity.

The form can vary, but the operating pattern is similar:

This layer is useful precisely because it is flexible.

A Telegram exchange can change wallets quickly. It can migrate channels. It can rename admins. It can move from one stablecoin chain to another. It can use new mule accounts. It can split larger flows across several counterparties. It can serve users who cannot or do not want to use regulated platforms.

For investigators, this makes Telegram exchanges difficult but valuable.

They often expose the operational layer behind the address.

Stablecoins turned informal crypto exchange into a cleaner business.

Bitcoin is volatile. Stablecoins are easier to quote.

A local dealer can quote:

No one has to price a volatile asset every few minutes. The dealer only needs a spread, a payment method, and available liquidity.

That is why stablecoin-heavy P2P and Telegram exchange activity matters for country-level attribution.

USDT, especially on low-cost networks like TRON, is widely used for fast settlement in informal liquidity routes. Elliptic has reported that large Telegram-based illicit marketplaces serving fraud networks in Southeast Asia used USDT as the primary payment method, with Huione Guarantee linked to at least $24 billion in transactions and Xinbi Guarantee linked to $8.4 billion.

Those examples are extreme. Most P2P and Telegram brokers are not operating at that scale.

But they show the broader point: chat-based crypto liquidity can become major financial infrastructure without looking like a normal exchange.

On-chain data shows addresses and flows.

Telegram groups can reveal:

This does not replace blockchain analysis. It enriches it.

A wallet that looks like an unknown address on-chain may become meaningful when it appears in a Telegram group offering USDT cash-out in a specific country.

A cluster that looks like generic high-volume stablecoin activity may become a local broker network once its handles, payment methods, and counterparties are mapped.

A P2P merchant may appear as one account inside a formal exchange, but operate across several chat groups outside it.

This is where OSINT and blockchain attribution need to meet.

The address is only one part of the evidence. The surrounding human infrastructure gives it context.

The formal crypto industry likes clean categories:

The local off-ramp world is less tidy.

A Telegram broker may act like an OTC desk for large trades, a P2P merchant for small trades, a remittance agent for cross-border settlement, and a liquidity source for local cash-out.

A P2P merchant on an exchange may also operate private Telegram deals.

An informal exchange group may use wallets at several centralised exchanges to manage liquidity.

A “broker” may simply be someone with verified accounts, local bank access, and enough stablecoin inventory.

For investigations, the question is not “which formal category does this entity belong to?”

The better question is:

What function does this actor perform in the flow of funds?

They may perform one or more functions:

This functional view is more useful than formal taxonomy.

Telegram-based crypto markets are adaptive.

When one group is removed, users can migrate. When one marketplace is disrupted, another can absorb activity. When admins are banned, replacement channels can appear. When a wallet is exposed, new wallets can be posted.

Reuters reported in May 2025 that Telegram shut down two major Chinese-language digital black markets, Xinbi Guarantee and Huione Guarantee, after they had reportedly facilitated more than $35 billion in transactions since 2021.

Elliptic later reported that after Huione Guarantee was shut down, merchants were encouraged to switch to another Telegram-based market called Tudou Guarantee, showing how quickly activity can attempt to relocate.

This is the core problem with static mapping.

A formal exchange usually has a domain, brand, legal entity, and infrastructure footprint. A Telegram market has looser boundaries. It may exist as channels, admins, merchant handles, wallet addresses, invite links, language communities, escrow relationships, and payment instructions.

To map it properly, investigators need to track both on-chain and off-chain signals.

P2P transactions are difficult because the fiat leg is not on-chain.

A simplified flow may look like this:

On-chain, investigators may only see:

They may not see:

That gap is where attribution weakens.

P2P and Telegram mapping help close it by tying wallets to actors, aliases, regions, payment rails, and repeated behavioural patterns.

P2P and Telegram exchanges are especially relevant where formal rails are weak or inconvenient.

This includes markets with:

In these markets, users may not ask, “Which regulated exchange is best?”

They ask:

Those questions shape the real off-ramp map.

The most important actor may not be the most visible platform. It may be the broker everyone uses.

You cannot map Telegram-based exchange activity the same way you map a centralised exchange.

A centralised exchange record may focus on:

A Telegram exchange record needs additional fields:

This record should clearly separate observation from verification.

For example:

That level of precision prevents overclaiming.

This distinction matters.

P2P and Telegram exchanges can be used for lawful purposes, especially in countries where formal banking and exchange infrastructure is weak.

People may use informal crypto brokers for:

But the same rails can also be exploited for:

The role of intelligence is not to label every informal broker as criminal.

The role is to map function, risk, evidence, and context.

A Telegram broker with transparent reputation, stable local payment methods, and normal retail flow is different from a broker advertising laundering services, mule accounts, scam cash-out, or anonymity guarantees.

The map should preserve that distinction.

P2P and Telegram exchange mapping should focus on recurring signals.

Important indicators include:

These signals do not automatically prove illicit activity. They guide prioritisation.

For a country-level attribution dataset, P2P and Telegram exchange coverage adds a layer that formal exchange mapping cannot provide.

It helps answer:

This is especially useful for:

Formal exchange attribution tells you where funds may have entered a known service.

P2P and Telegram mapping tells you how funds may have moved into local liquidity.

Crypto investigations are cleanest on-chain.

They become harder at the edge.

That edge is where a wallet becomes a person, broker, merchant, mule account, bank transfer, mobile wallet, cash pickup, or Telegram handle.

P2P and Telegram exchanges live at that edge.

They are not always visible in formal registries. They may not have websites. They may not have compliance departments. They may not expose stable infrastructure. But they can still move large volumes, connect users to local fiat, and act as the practical off-ramp in markets where formal exchange coverage is incomplete.

The investigation does not end when funds leave the blockchain graph.

Often, that is where the most important map begins.

The real question is not only:

Which exchange did the funds reach?

It is:

Who turned the crypto into local money?

That is the hidden role of P2P and Telegram exchanges.

Wallet labels are useful. But in emerging markets, they often fail because the real crypto economy does not fit neatly into global exchange categories.

A wallet label can make blockchain analysis feel more certain than it really is.

An address gets tagged as an exchange.

A cluster gets attached to a known platform.

A service gets grouped under one entity name.

A transaction graph suddenly looks cleaner.

That is the promise of wallet labelling: turning raw blockchain addresses into named infrastructure.

But in emerging markets, the picture is rarely that simple.

Crypto activity often moves through a messy mix of local exchanges, offshore platforms, P2P merchants, Telegram brokers, fintech apps, gambling platforms, OTC desks, remittance agents, payment processors, mule accounts, and deposit-only services.

Some of these actors have formal names and public websites. Many do not. Some use centralised exchanges as backend liquidity. Some rotate wallets constantly. Some operate across multiple countries. Some are only visible through local apps, language-specific groups, or payment instructions inside private chats.

A global wallet label may catch the visible part of the flow.

It often misses the local logic behind it.

That is why wallet labels fail in emerging markets.

Most attribution datasets are strongest where the infrastructure is most visible.

Large global exchanges are easier to identify. They have high-volume wallet clusters, public domains, support pages, compliance teams, and consistent infrastructure patterns. Their wallets appear in many investigations, which gives analysts more chances to confirm and refine labels.

Emerging-market activity is different.

A user in India, Pakistan, Vietnam, Brazil, Nigeria, Turkey, Thailand, Argentina, or South Africa may use a major exchange, but they may also rely on local brokers, P2P merchants, domestic payment apps, remittance shops, offshore exchanges, or informal stablecoin dealers.

Chainalysis’ 2025 Global Crypto Adoption Index ranked India first, followed by the United States, Pakistan, Vietnam, and Brazil, showing that high adoption is not limited to mature Western markets or neatly regulated exchange ecosystems.

That matters for attribution.

A dataset that performs well on Coinbase, Binance, Kraken, OKX, and Bybit may still be weak at identifying a regional broker in Lagos, a Telegram USDT dealer in Istanbul, a small app in São Paulo, or a P2P merchant serving users in Bangkok.

The global exchange label is useful.

It is not the whole map.

In many markets, the named exchange is not the final intelligence object.

A P2P merchant may use a Binance account. A Telegram broker may source liquidity through OKX. A remittance desk may settle through a local exchange. A small fintech app may use a third-party custodian. A gambling platform may deposit into a larger exchange cluster. A local OTC desk may hold balances across several venues.

On-chain, these flows can collapse into the same familiar labels.

The graph may show funds moving to a major exchange. But the practical actor may be a broker, merchant, mule network, or local cash-out operator using that exchange as infrastructure.

This creates an attribution problem.

The label may be technically correct at one layer, but operationally incomplete.

If the wallet is labelled only as a major exchange, the analyst may miss the local actor who controlled the account, coordinated the deal, received the fiat, or provided the cash-out route.

In emerging markets, the useful question is often not only:

Which platform did the funds touch?

It is:

Who was using that platform as local liquidity infrastructure?

P2P markets create a structural problem for wallet labelling.

In a normal exchange deposit flow, a user sends crypto to a deposit address controlled by the exchange. In a P2P flow, the user may be interacting with another person or merchant, while the platform only provides escrow, reputation, chat, or account infrastructure.

The fiat leg happens outside the blockchain.

A buyer receives USDT. A seller receives local currency through a bank transfer, mobile wallet, cash deposit, or payment app. The blockchain sees the crypto movement, but not the domestic settlement.

This makes labels weaker.

A wallet may belong to a merchant, but the merchant may operate across several platforms. A deposit may be credited inside a centralised exchange, but the economic purpose was a local cash-out. A wallet may look like a personal address, but function as a broker’s working capital wallet.

In markets where P2P is a major liquidity layer, exchange labels alone can hide the real off-ramp.

The address label tells you where the crypto moved.

It does not always tell you how local value changed hands.

Stablecoins made informal exchange activity easier to scale.

A local broker does not need to quote volatile Bitcoin prices all day. They can quote USDT against local currency, take a spread, and settle through domestic payment methods.

This is one reason stablecoin activity has become central to emerging-market crypto use. TRM Labs reported that stablecoins made up 30% of all on-chain crypto transaction volume in 2025, with annual volume reaching more than USD 4 trillion by August 2025. FATF’s 2025 report also noted that fiat-backed stablecoins dominated the stablecoin market, representing 95% of total market capitalisation in October 2025.

For wallet labels, this creates a problem.

High-volume USDT activity may pass through centralised exchanges, self-custody wallets, brokers, P2P merchants, payment intermediaries, and local settlement desks. Some of these are labelled. Many are not.

A stablecoin broker may not have a formal platform name. The “entity” may be a Telegram handle, a WhatsApp number, a repeated bank account, a group admin, or a wallet posted across multiple channels.

Traditional wallet labels are built around identifiable services.

Emerging-market stablecoin liquidity is often built around repeat operators.

That mismatch is where labels fail.

Most global attribution datasets are biased toward what can be repeatedly observed at scale.

That means large exchanges, major bridges, mixers, gambling platforms, and high-profile services get better coverage. Smaller country-specific venues often receive weaker coverage, especially if they operate in local languages, serve only domestic users, require local KYC, or support payment methods that are invisible from outside the market.

This creates predictable blind spots.

A platform may be popular locally but almost invisible globally. A broker may be well known in a Telegram group but absent from a standard VASP list. A fintech app may support crypto deposits indirectly but not present itself as a crypto exchange. A licensed venue may support only a narrow set of rails, while an offshore or informal operator handles far more actual liquidity.

In these cases, the absence of a label does not mean the absence of an entity.

It may only mean the entity sits outside the usual collection path.

Many emerging-market crypto services are difficult to map remotely.

A researcher outside the country may not see the same interface as a local user. Registration may require a domestic phone number. KYC may require national ID. Fiat withdrawals may require a local bank account. P2P markets may display different merchants depending on currency, region, and account status. Some apps may only be available in local app stores.

This affects wallet labels directly.

If an analyst cannot access the local account flow, they may never see the deposit address, payment rail, or withdrawal path that local users actually use.

A support page may claim a rail exists, but only live access proves whether it works. The opposite can also happen: public documentation may be weak, but the rail appears inside the local app after verification.

This is why country-level testing matters.

A wallet label produced from outside the market may be correct in a broad sense, but still miss the account-level infrastructure that local users see.

Even when wallet labels are correct, they are not permanent.

Exchanges rotate deposit addresses. Platforms change custodians. Chains are suspended. Stablecoin rails are added or removed. Withdrawal rules change. KYC requirements tighten. Payment processors are replaced. Apps rebrand. Local operators migrate from one wallet to another.

FATF’s 2025 targeted update on virtual assets and VASPs highlighted continued gaps in global implementation of Recommendation 15, even as jurisdictions with materially important VASP activity made progress in regulation and supervision. That uneven regulatory environment creates constant infrastructure movement. Platforms adapt to local rules, banking relationships, enforcement pressure, and compliance obligations.

In emerging markets, this movement can be faster and less visible.

A label that was accurate six months ago may now be stale. The address may still exist on-chain, but no longer represent active deposit infrastructure. A platform may still operate, but through different rails. A broker may still trade, but from a new wallet. A P2P merchant may still be active, but under a different handle.

A static wallet label cannot capture this unless it includes freshness metadata.

Without a verification date, a label is incomplete.

This is one of the biggest weaknesses.

A wallet label usually identifies an entity. But investigations often need to understand a route.

For example, a transaction may involve a local user sending USDT to a broker, the broker consolidating funds into a centralised exchange, and fiat being paid out through a domestic bank transfer. A basic label may only show the centralised exchange.

That is not wrong.

It is just not enough.

The useful route includes the broker, the payment method, the fiat currency, the local country context, the exchange account used for liquidity, and the chain used for settlement.

A venue label answers:

Who controls this wallet or cluster?

A route map answers:

How did value move from crypto into local money?

Emerging-market investigations often need the second answer.

An unknown address forces caution.

A labelled address can create confidence.

That confidence is useful when the label is fresh, precise, and evidence-backed. It is dangerous when the label is stale, broad, or missing local context.

A label like “Exchange” can hide many realities. It may represent a user deposit address, a hot wallet, a third-party custodian, a payment processor, a broker-controlled account, or a regional entity operating under the same brand. It may also represent historical infrastructure that is no longer active.

This can lead to weak conclusions.

An investigator may assume funds reached a compliant exchange when they actually reached an informal broker using that exchange. A compliance system may reduce alert priority because the destination appears familiar. A dataset may undercount exposure to local high-risk services because their flows end inside large exchange clusters.

False confidence creates analytical debt.

It makes bad assumptions look clean.

The fix is not to abandon wallet labels.

The fix is to make them more evidence-backed, local, and time-aware.

A stronger label should include more than an entity name. It should explain how the label was established, when it was last verified, what account conditions applied, which asset and chain were tested, and whether the wallet was linked through direct platform access, transaction evidence, public documentation, OSINT, or behavioural clustering.

For emerging markets, the evidence model should also include local context.

That means capturing whether the address was observed through a local verified account, a P2P merchant flow, a Telegram broker post, a fintech app deposit screen, a gambling platform, an OTC desk, or a remittance route.

A useful record should separate:

This is not just cleaner documentation.

It gives downstream analysts a way to judge how much trust to place in the label.

Wallet labels are only one layer.

The stronger model combines wallet attribution with access intelligence.

That means asking not only which address belongs to which service, but what a user can actually do through that service in a specific market. Can they deposit USDT? Which chain? Can they withdraw crypto? Can they cash out to local bank transfer? Does P2P appear after KYC? Is the rail available to residents only? Is the account deposit-only? Does the platform auto-convert crypto into fiat balance?

This kind of intelligence is harder to collect, but much more useful.

It turns a label from a static tag into a working record of operational access.

For emerging markets, that is the difference between naming infrastructure and understanding it.

Wallet labels fail in emerging markets because emerging-market crypto activity is not only exchange activity.

It is local, fragmented, adaptive, and often mediated through human liquidity networks.

The real ecosystem includes exchanges, P2P merchants, Telegram brokers, OTC desks, fintech apps, payment processors, gambling platforms, remittance agents, domestic banks, mobile wallets, and cash routes. Some are formal. Some are informal. Some are visible globally. Many are not.

A basic wallet label may tell you where funds touched known infrastructure.

It may not tell you who controlled the local route, which payment method was used, whether the rail is still active, whether the platform works in that country, or whether the label is current.

For investigations, that missing context matters.

The question is not only:

What is this wallet labelled as?

It is:

What role does this wallet play in the local movement of value?

That is the question emerging-market attribution has to answer.

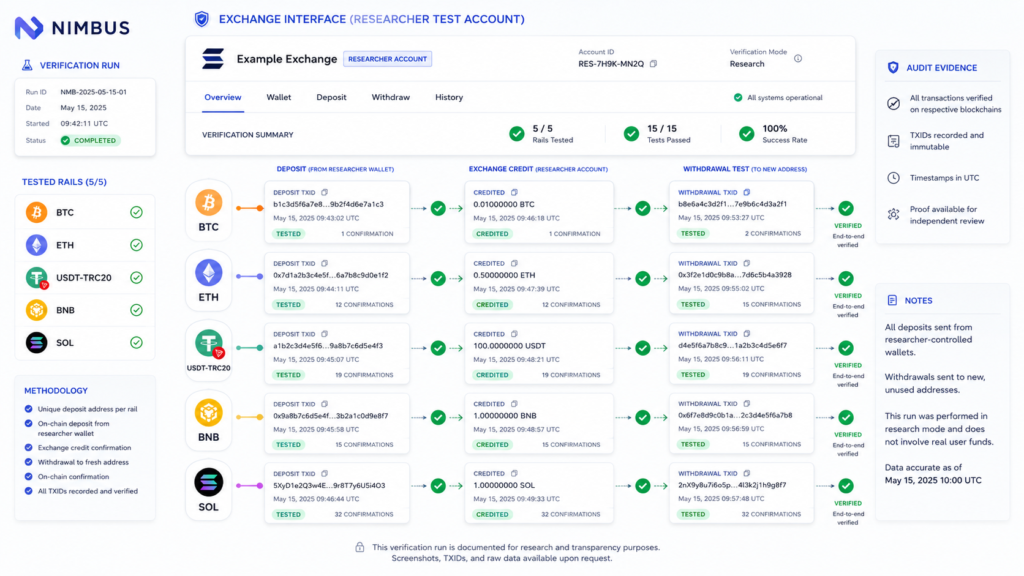

Primary-rail verification is not a full audit of a crypto venue. It is targeted proof that a platform can generate, receive, credit, and sometimes withdraw through the most important transaction rails.

Crypto attribution always involves a trade-off between depth, speed, cost, and coverage.

A full verification cycle across every chain, asset, KYC tier, account type, and withdrawal method can become expensive quickly. Every additional network adds more work: account setup, local access, deposit testing, withdrawal testing, screenshots, transaction fees, network fees, failed attempts, retries, minimum deposits, and sometimes lost funds on deposit-only platforms.

That is why many investigations use a primary-rail model.

Instead of testing every possible asset and network, the researcher focuses on the rails most likely to matter for attribution, off-ramp mapping, and investigative utility.

These usually include:

Primary-rail verification does not prove everything. But when done properly, it proves something valuable: that a venue is operationally reachable through specific live rails, under specific account conditions, at a specific point in time.

That is far stronger than a public claim, old label, or scraped directory.

A platform appearing in a public directory does not prove it is operational.

A website may still load even if trading is dead. An app may exist even if deposits are disabled. A support page may list chains that no longer work. A platform may claim country availability but block users during KYC. An exchange may show crypto balances but prevent withdrawals. A local broker may advertise USDT support but fail to provide a usable address.

Primary-rail verification tests whether the venue actually works.

At a basic level, it shows whether a real account can access the platform, whether the platform can generate a deposit address, whether a selected asset and chain are visible, whether a micro-deposit can be sent, and whether the balance is credited after confirmation.

That moves the record from:

“This venue exists.”

To:

“This venue was operationally verified on this rail.”

For attribution work, that difference matters.

Wallet attribution decays because venues rotate addresses, change custody providers, update infrastructure, disable chains, or migrate users to new wallets.

A primary-rail test creates fresh evidence. It can show the current deposit address displayed to a verified account, the asset and chain linked to that address, the account context in which it appeared, and whether funds were actually credited after a test deposit.

This is the core value.

A blockchain label without recent verification is only historical intelligence. It may still be useful for older investigations, but it should not be treated as proof of current infrastructure.

Primary-rail verification refreshes the attribution layer.

It answers a simple but important question:

Can we prove this venue still exposes this rail today?

A deposit address is useful, but it is not enough by itself.

The verification record should also explain the conditions under which that address became visible. This includes the country of access, account type, KYC tier, documents required, local phone or bank requirements, resident or non-resident status, and whether the rail appeared before or after verification.

This matters because crypto venues do not expose the same infrastructure to every user.

A rail may be available only after email verification, phone verification, basic KYC, enhanced KYC, proof of address, local ID verification, business account approval, domestic bank linking, or manual risk review.

Without access-condition metadata, the attribution is weaker.

A deposit address alone says:

“This rail exists.”

A stronger record says:

“This rail exists for this type of user, in this country, at this verification level, on this date.”

That is much more useful for investigators, compliance teams, and analytics vendors.

Deposit address generation is useful. But a generated address does not prove that the rail works.

A stronger test proves the platform can actually receive funds. That means the platform generated a valid address, a micro-deposit was sent, the transaction confirmed on-chain, and the platform credited the user balance.

This turns a static address into an evidence-backed attribution point.

It also separates real rails from interface noise. Some platforms show deposit options that fail when used. Some generate addresses but do not credit funds. Some support a chain technically but have broken monitoring. Some require minimum deposits, and anything below the threshold may not appear in the account.

Primary-rail deposit testing exposes these problems.

This is why “deposit address observed” and “deposit credited” should be treated as different evidence levels.

This is where precision matters.

Primary-rail verification does not automatically prove two-way functionality unless withdrawal testing is included.

There are three different levels of evidence:

These are not the same.

A platform may support deposits but not withdrawals. It may support withdrawals only after higher KYC. It may support crypto deposits but fiat-only withdrawals. It may auto-convert crypto into local balance. It may impose minimum withdrawal limits that make testing expensive. It may also hold withdrawals for manual review.

So the wording matters.

A primary-rail test should say “deposit rail verified” when only the deposit was tested. It should say “withdrawal visible but not tested” when the interface shows a withdrawal option but no outbound transaction was performed. It should say “withdrawal verified” only when funds were successfully withdrawn and an outbound TXID was captured.

It should not say “full rail verified” unless both deposit and withdrawal were tested.

That protects the dataset from overclaiming.

Not every chain has equal investigative value.

A venue may technically support dozens of assets. But most investigation and off-ramp work focuses on the rails that carry meaningful liquidity.

Primary rails are selected because they tend to be high-volume, widely supported, common in exchange deposits, useful for tracing major flows, relevant to stablecoin cash-out, and cost-effective to test.

USDT on TRON often matters because it is cheap, fast, and widely used in P2P and broker activity. BTC and ETH matter because they remain foundational rails. BNB and SOL may matter depending on regional exchange behaviour and user demand.

Primary-rail verification proves that the venue has live access on the rails most likely to matter.

It does not prove the venue has no other rails.

It proves that the selected rails were tested and observed.

That distinction is important.

Primary-rail verification is not the same as full-depth mapping.

It does not prove every supported chain, every supported token, every deposit method, every withdrawal method, every fiat payout option, every KYC tier, every regional account variation, every business feature, or every temporary edge case.

A venue may support additional networks that were not tested. These could include Polygon, Avalanche, TON, XRP, XLM, DOGE, Litecoin, BCH, Arbitrum, Optimism, Base, or local stablecoin rails.

If those networks were outside the test scope, the report should say so clearly.

A good primary-rail report should separate:

This keeps the output honest.

It also helps clients understand the difference between tested proof and broader coverage claims.

Primary-rail verification is timestamped evidence.

It proves what was true during the test window. It does not prove that the same rail will remain active forever.

A venue can later rotate deposit addresses, suspend a chain, change custody providers, increase KYC requirements, disable withdrawals, remove a token, change minimum deposits, block a country, replace payment processors, introduce Travel Rule checks, or move to new wallet infrastructure.

This is why every record needs freshness metadata.

The stronger claim is not:

“This venue supports USDT-TRC20.”

The stronger claim is:

“USDT-TRC20 deposit was verified for this venue under these account conditions on this date.”

That is a cleaner intelligence statement.

It gives the reader both the finding and the limits of the finding.

Primary-rail verification is infrastructure evidence. It is not a full risk assessment.

It does not automatically prove that a platform is compliant, non-compliant, high-risk, safe, licensed, exposed to suspicious flows, or knowingly serving illicit actors.

It proves access, rails, and transaction behaviour under tested conditions.

Risk interpretation requires additional evidence. That may include regulatory status, licensing records, transaction exposure, known illicit counterparties, sanctions screening, scam reports, dark-market links, P2P merchant behaviour, Telegram group links, or internal compliance posture if available.

Primary-rail verification is one layer.

It should feed into risk analysis, not replace it.

A venue can be known without any route being verified.

A platform may appear in a regulator’s list. It may be mentioned in media. It may have a public website. It may have an app. It may claim to support crypto. It may appear in older datasets.

None of that proves current rails.

Primary-rail verification creates a different category: a verified route.

A verified route connects a specific platform, asset, chain, account type, access tier, test date, evidence set, and transaction result.

That is more valuable than entity discovery alone.

For Nimbus-style outputs, this distinction should be explicit. A discovered entity has been identified as relevant, but not yet tested. An accessible entity has confirmed account access. A deposit-verified entity has generated and credited a tested deposit. A withdrawal-verified entity has produced an outbound transaction. A fiat-observed entity has visible local payout methods, even if those were not tested.

This avoids confusion between coverage and proof.

Attribution confidence depends on evidence quality.

Weak confidence may come from public claims, user reports, old screenshots, third-party lists, unverified wallet labels, historical address clusters, or interface-only observations.

Stronger confidence comes from live account access, fresh deposit address generation, successful micro-deposits, confirmed crediting, outbound withdrawal TXIDs, timestamped screenshots, KYC-tier documentation, repeated observations, and consistency with known wallet infrastructure.

Primary-rail verification improves confidence because it creates direct evidence.

It links the platform interface to the blockchain transaction.

That link is the attribution bridge.

Full-depth verification is useful, but it is not always necessary for every market, every platform, or every client need.

Primary-rail verification gives a practical middle path.

It is especially useful when the goal is to confirm whether a venue is operational, refresh stale attribution, verify the most important rails, map priority exchanges in a market, identify deposit-enabled services, test stablecoin cash-out relevance, build a country-level intelligence baseline, or decide which venues deserve deeper investigation.

This makes it a strong first-pass model for country mapping.

A client may not need every altcoin rail verified immediately. They may first need to know which venues are active, which primary rails work, and which platforms deserve deeper follow-up.

Primary-rail verification provides that first layer of proof without pretending to be exhaustive.

A clean verification record should include enough detail for another analyst to understand exactly what was proven.

It should identify the venue, domain or app, country context, and entity type. It should explain the account context, including account country, user type, KYC tier, verification requirements, and access limitations.

It should also record the asset and network tested, whether the test involved deposit, withdrawal, or both, and any relevant minimum deposit, withdrawal, or fee constraints.

The evidence layer matters most. A strong record should include deposit address screenshots, TXIDs, credited balance screenshots, withdrawal screenshots where relevant, outbound TXIDs where tested, and clear timestamps.

The result should be written plainly. Was the address generated? Was the deposit sent? Was it credited? Was withdrawal visible? Was withdrawal completed? Was the rail blocked, failed, or out of scope?

Analyst notes should capture the messy parts: KYC constraints, broken flows, manual review, deposit-only behaviour, auto-conversion, local payment observations, and suggested re-test window.

This is what makes the dataset auditable.

Primary-rail verification proves that a specific venue, under specific account and jurisdictional conditions, exposed or processed specific high-value crypto rails during a specific test window, with evidence linking the platform interface to on-chain activity.

That is the clean claim.

Not more. Not less.

It does not prove total platform coverage. It does not prove permanent support. It does not prove every chain. It does not prove every user type. It does not prove platform-wide risk by itself.

But it does prove something far stronger than a scraped list or inherited label.

It proves live operational access on the rails that matter most.

Crypto investigations fail when they rely on stale or shallow labels.

A wallet may have been correctly attributed years ago but no longer represent active infrastructure. A platform may be listed in public directories but no longer credit deposits. A venue may support USDT on paper but not in a tested local account. A deposit address may exist, but withdrawals may be blocked. A cash-out path may require higher KYC.

Primary-rail verification reduces that uncertainty.

It helps investigators understand whether a platform is active, which major rails are live, whether funds can be credited, whether withdrawals are visible or tested, what KYC tier is required, what country access conditions apply, and whether the attribution is current.

For wallet attribution, country mapping, exchange intelligence, off-ramp discovery, VASP discovery, Travel Rule enrichment, dataset refreshes, and investigation triage, that is a useful proof layer.

The point is not to claim exhaustive knowledge.

The point is to replace assumptions with tested evidence.

Primary-rail verification does exactly that.

Crypto does not become useful when it is bought. It becomes useful when it can move back into the local economy.

Most blockchain attribution work starts with exchanges. That makes sense. Centralised exchanges are visible, high-volume, and easier to categorise than the fragmented networks around them. They have deposit addresses, withdrawal flows, compliance teams, public domains, app interfaces, and often a formal relationship with regulators.

But in many markets, exchanges are only the cleanest part of the picture.

Real-world cash-out behaviour often moves through a wider off-ramp ecosystem: local brokers, P2P merchants, fintech apps, mobile money, OTC desks, remittance shops, payment processors, gambling platforms, tokenised investment apps, informal Telegram liquidity groups, and region-specific wallet services.

If you only map exchanges, you map the obvious layer.

If you want to understand how crypto actually leaves the chain and enters local economies, you need to map the local off-ramp layer.

A centralised exchange can convert crypto into fiat, but it is not always the route people use.

In emerging markets, users often care less about whether a platform is globally recognised and more about whether it solves the final-mile problem:

Mastercard’s explanation of crypto on-ramps and off-ramps defines an off-ramp as the process of moving crypto or stablecoins into fiat-denominated goods, services, cards, or bank accounts. That definition matters because off-ramping is not limited to exchange order books. It includes the wider conversion layer between crypto balances and real-world spending power.

For attribution teams, the risk is simple: if the map only includes exchanges, it may miss the actual exit route.

A formal exchange is easy to name. A functional off-ramp is harder.

A local off-ramp may be:

Some of these entities are licensed. Some are semi-formal. Some are simply operationally important because users trust them, liquidity exists there, and money actually moves.

This is the difference between regulatory taxonomy and intelligence taxonomy.

Regulators may classify entities as VASPs, payment providers, brokers, money service businesses, gambling operators, fintechs, or unlicensed actors. Investigators need a second question: does this entity provide a practical crypto-to-fiat path in this market?

That is the off-ramp question.

P2P cash-out is often described as a product feature inside exchanges. That framing is too narrow.

In practice, P2P behaves like distributed local liquidity infrastructure. A user sells crypto to another user, receives local currency through a bank transfer, mobile money, wallet app, or other domestic payment method, and the crypto stays inside the platform or moves to the merchant’s wallet.

Recent primers on off-ramping describe P2P services as a way for users to sell crypto directly to another person in exchange for fiat, often using local payment apps and currencies. They also note that the model is less regulated and can be exploited by bad actors.

For blockchain intelligence, this creates a problem.

The on-chain movement may only show a deposit into a platform, merchant wallet, or intermediary address. The fiat leg happens off-chain, inside domestic payment rails. Unless the off-ramp actor is identified, the transaction graph stops too early.

This is why local P2P merchant mapping matters.

It can reveal which merchants are active, which payment methods they support, which currencies they serve, which venues they use, and whether they act as repeat liquidity points.

Bitcoin used to dominate many illicit and grey-market crypto flows. That is no longer the whole story.

Chainalysis’ 2025 crypto crime reporting notes that some categories, such as ransomware and darknet markets, remain Bitcoin-heavy, while other activity, including scams and laundering, increasingly spreads across a broader set of asset types.

Stablecoins changed the local off-ramp problem because they are easier to price, easier to quote, and often better suited for cross-border and emerging-market use cases. A local broker can quote USDT to naira, pesos, reais, rupees, lira, baht, dong, dirhams, or rand without needing users to manage Bitcoin volatility.

Fintech infrastructure providers also increasingly describe stablecoin off-ramps as a way to convert stablecoins into local currency and withdraw to bank accounts or mobile money.

That means the relevant off-ramp map is not only “which exchanges support BTC withdrawals?”

It is also:

Stablecoin liquidity has made the local layer more important, not less.

A narrow VASP list is useful, but incomplete.

FATF’s updated recommendations continue to focus on anti-money laundering and counter-terrorist financing standards for virtual assets and virtual asset service providers. But the practical cash-out ecosystem in many countries includes actors that do not always look like cleanly registered crypto exchanges.

For intelligence and compliance use cases, the map should include several layers.

Licensed exchanges

These are the obvious entities: regulated local exchanges, approved brokers, and compliant trading platforms.

Globally accessible exchanges

These may not be locally licensed but can still serve users in the country through cards, P2P markets, crypto deposits, or local payment methods.

P2P markets and merchants

These are often critical in countries where banking access is fragmented, capital controls exist, or users prefer stablecoin liquidity over exchange order books.

Fintech and payment apps

Some apps integrate crypto directly. Others touch crypto indirectly through partners, payment processors, or stablecoin infrastructure.

OTC brokers and local liquidity desks

These matter for higher-volume flows, business users, remittance corridors, and informal settlement.

Gambling, gaming, and high-risk payment rails

These can act as practical conversion points, especially when deposits and withdrawals bridge crypto and fiat.

Remittance and cash agents

In some corridors, crypto is not the user-facing product. It is the settlement layer behind local payout.

This broader map is less tidy than an exchange list. It is also more useful.

A weak off-ramp map asks: who accepts crypto?

A stronger off-ramp map asks:

This is where desk research fails.

A website may claim to support crypto. The app may show a deposit button. The interface may list USDT. But after account creation, the picture can change. KYC may block access. The deposit address may not generate. Withdrawals may be disabled. Local bank transfer may be available only after higher verification. Some rails may appear in the interface but fail during execution.

Off-ramp mapping needs live testing, not only public data.

A common mistake is ignoring deposit-only platforms because they do not support crypto withdrawals.

That is too simplistic.

A deposit-only platform can still be important if crypto enters the service and value exits through fiat, vouchers, betting balances, merchant payments, local bank transfer, prepaid cards, or app credits.

From a blockchain perspective, these platforms may look like sinks. Funds go in and do not come back out on-chain. But from an investigative perspective, that may be exactly why they matter.

The question is not only whether crypto can be withdrawn.

The question is whether crypto can be converted into local value.

A platform that accepts USDT and pays out in local currency may be more relevant to cash-out mapping than a small exchange with on-chain withdrawal support but no meaningful local liquidity.

Global datasets tend to overrepresent visible global exchanges and underrepresent local actors.

That creates blind spots in countries where users rely on regional apps, small brokers, P2P merchants, remittance rails, and fintech workarounds.

The blind spot is not only about missing names. It affects transaction interpretation.

Without local off-ramp context, an analyst may see a transfer to an unfamiliar address and classify it as unknown. But locally, that address may belong to a popular broker, a P2P merchant, a remittance-facing platform, or a deposit processor used by multiple apps.

This is especially important in markets with:

In these markets, the local map is not optional. It is the core intelligence layer.

A good off-ramp record should not just say “Platform X is active in Country Y.”

It should capture evidence.

At minimum:

The strongest datasets separate public claims from tested access.

That distinction prevents overconfidence.

“Website says USDT supported” is not the same as “local verified account generated a TRC20 deposit address on 7 May 2026, deposit confirmed, balance credited, withdrawal to local bank option visible after KYC.”

The second record is intelligence. The first is a lead.

Exchange-first mapping starts with a list of known venues and asks where they operate.

Country-first mapping starts with a market and asks how crypto actually converts into local value there.

That shift changes the investigation.

In a country-first model, the analyst does not only ask, “Which exchanges are licensed here?”

They ask:

This approach is messier. It also matches reality.

A local off-ramp map is not a neat compliance directory. It is a working model of how value exits crypto in a specific country.

For compliance teams, local off-ramp mapping improves alert triage, entity enrichment, and exposure analysis.

For investigators, it helps identify where funds may have exited into fiat.

For Travel Rule and VASP discovery teams, it reveals entities that may not appear in standard global registries.

For blockchain analytics vendors, it improves coverage in markets where global exchange lists are too shallow.

For law enforcement and threat intelligence teams, it helps convert on-chain leads into local investigative leads.

The value is not just better labels. It is better operational context.

A wallet address attached to a known global exchange tells one story. A wallet address tied to a local broker, P2P merchant, or deposit-only fintech route tells another.

Blockchain intelligence often begins with on-chain clustering. But the economic meaning of a flow depends on what happens at the edge of the chain.

That edge is local.

A user in Lagos, Bangkok, São Paulo, Istanbul, Ho Chi Minh City, Dubai, Nairobi, Manila, or Buenos Aires may not cash out through the same route shown in a global exchange directory. They may use a local merchant, a P2P desk, an app, a payment processor, a regional broker, or a venue that is invisible to most global datasets.

That is why off-ramp mapping needs to go beyond exchanges.

The real question is not only:

Which exchanges operate in this country?

It is:

How does crypto become usable local money here?

That is the map that matters.